Low doc home loans let self-employed Australians buy, refinance or invest in residential property without lodging two years of tax returns. Instead of payslips and full financials, lenders assess your income through BAS statements, business bank statements or a signed accountant’s declaration.

They suit sole traders, contractors, company directors and investors whose real income doesn’t show up cleanly in standard bank documentation. That happens when income is spread across entities, when financials are behind, or when the business is simply too new.

At Formation Finance we match the scenario to lender policy before lodgement, not during credit assessment. That is the single biggest difference between a low doc application that settles and one that stalls.

Rates from 5.99% p.a.# (6.29% p.a. comparison rate*) • Up to 80% LVR • Refinance cashback up to $2,000**

# Actual rate depends on lender criteria, LVR and your circumstances. Rates as at 29 July 2026, indicative only, subject to change. • * Comparison rate based on $150,000 loan over 25 years. WARNING: This comparison rate is true only for the example given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. • ** Cashback subject to lender criteria and minimum loan size. • *** Interest Only subject to LVR restrictions and higher rates. • ## Foreign income subject to country, currency and visa status; lower LVR caps apply. • + Credit impairment case-by-case; LVR and rate loadings apply. • ^ Other fees may apply. Specific fees confirmed in your loan offer. • ^^ Additional valuation costs may apply for properties >$1.5M or in regional locations. • All applications subject to credit assessment.

A low doc home loan is a residential mortgage assessed on alternative income evidence rather than tax returns. “Low doc” does not mean no documentation. It means the documentation is different.

The loan itself is structurally identical to a standard home loan. Same principal and interest repayments, same 30-year terms, same offset and redraw features. What changes is how the lender establishes that you can service it.

Under responsible lending obligations, a lender still has to reasonably verify your income. A low doc product satisfies that obligation with a self-declaration of income supported by at least one independent document, most commonly BAS, business bank statements, or an accountant’s letter.

Because the verification is indirect, lenders price in additional risk. Expect a rate premium over full doc, a lower LVR cap, and in most cases lenders mortgage insurance above 60% LVR.

Low doc suits borrowers whose income is genuine but hard to evidence the standard way.

You’ll generally need:

A straight answer. If you can produce full financials, a full doc loan will almost always price better. We will tell you that rather than sell you a low doc.

No single document carries an application. The documents, the borrower and the security property have to tell one consistent story. Where the sources contradict each other the file stalls, no matter how strong any individual document looks.

BAS statements

Usually the last 4 quarters lodged with the ATO. Lenders read them for turnover, trading consistency and whether lodgements are current. Late or amended BAS is a red flag. A genuine seasonal dip explained upfront is not.

Business bank statements

Typically 6 months, sometimes 12. Lenders check deposit patterns, whether declared income actually lands in the account, and whether the account runs clean. That means no dishonours, no habitually overdrawn balances, no undisclosed loan repayments.

Accountant’s declaration

A signed letter from a qualified accountant confirming your income position. It carries most weight when your structure needs explaining rather than listing, such as multiple entities, retained earnings, trust distributions or a recent restructure. A one-line letter stating a figure is far weaker than one showing how the figure is derived.

Self-declaration of income

Required by every low doc lender. It has to be consistent with whichever supporting document you supply. A declared figure materially above what the BAS or bank statements support is the most common single cause of decline.

Some lenders call this product low doc, others call it alt doc. They are not identical. Alt doc generally requires more income evidence and prices better for it.

| Low Doc | Alt Doc | |

|---|---|---|

| Income evidence | Self-declaration + 1 supporting document | Self-declaration + 2 or more |

| Typical documents | BAS or bank statements or accountant letter | BAS and bank statements, often plus accountant letter |

| Max LVR | Up to 80% | Up to 80-85% ⚠️需核实 |

| Rate | Premium over full doc | Usually better than low doc |

| Best when | You have one solid income document | You have two |

The practical rule. If you can produce two independent income documents, ask about alt doc before you accept a low doc rate. The paperwork difference is small and the pricing difference is not.

If your tax returns are current, a full doc loan will price better again. If you have no income documentation at all and the deal is time critical, see No Doc Loans.

We assess your documents, business structure and target loan against current lender policy, then shortlist only the lenders whose policy your scenario actually fits.

What we need from you: ABN details and trading history, an indication of your income position, whichever supporting documents you already hold, and your deposit or equity position.

What you receive: a shortlist of lenders that fit, an indicative rate and LVR, and a written list of exactly which documents to gather. If a full doc loan would serve you better, we say so at this stage.

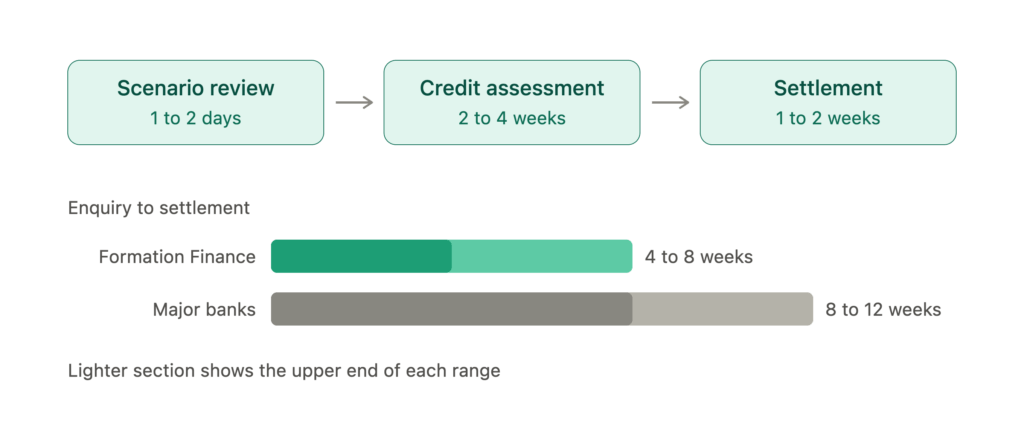

The application is lodged once, complete, with the lender selected at stage one. Valuation is ordered and conditions are handled as they arise rather than accumulating.

What we need from you: signed application and privacy consent, the income documents identified at stage one, and identification.

What you receive: conditional approval, then formal approval once valuation and conditions clear.

Loan documents are issued and signed, your solicitor or conveyancer is instructed, and funds settle.

What we need from you: signed loan documents and your solicitor’s details.

What you receive: settlement, and a written summary of your loan structure, rate and review date.

Reviewed by Jackie Wang, Partner at Formation Finance

Jackie Wang holds a Master of Professional Accounting from the Royal Melbourne Institute of Technology (RMIT), and has over 10 years of experience in finance and lending, structuring tailored low doc home loan solutions for Australian borrowers and self-employed clients.

Last update: 29/07/2026

A low doc (or lo doc) loan is a type of mortgage designed for self-employed borrowers who can’t provide standard documentation like tax returns or payslips. Instead, income is verified through BAS, bank statements, or an accountant’s declaration.

Low doc loans are ideal for self-employed individuals, sole traders, freelancers, or small business owners with irregular income or recently established businesses.

Generally up to 80% of the property value.

Absolutely. Many self-employed borrowers use low doc loans to refinance existing debt, consolidate personal or business loans, or access equity from their property.

Yes. We understand self-employed people may have complicated financials that their accountant is best placed to understand and articulate.