Home - Services - Land Loans

At Formation Finance, our land loans are tailored to help individuals and developers secure funding for vacant land purchases. Also known as land finance, these loans are typically secured against the land itself and are ideal for bridging the gap between acquisition and the start of construction.

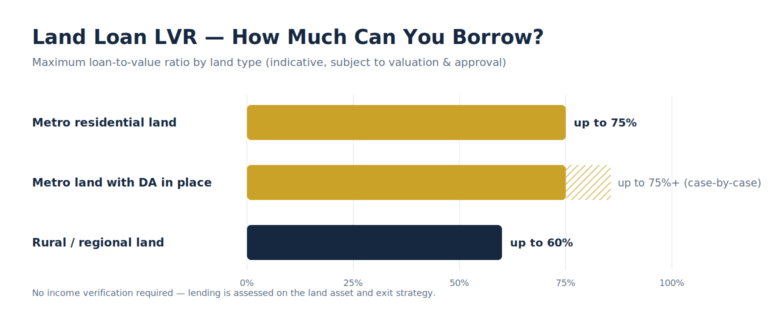

Our flexible land loan solutions turn raw sites into real opportunities. Whether you’re land banking in Sydney’s growth corridors, refinancing a development site on the Gold Coast, or unlocking equity from unused land in Melbourne, we provide up to 75% LVR with loan terms from 3 to 24 months—crafted to suit your project, not constrained by traditional bank criteria.

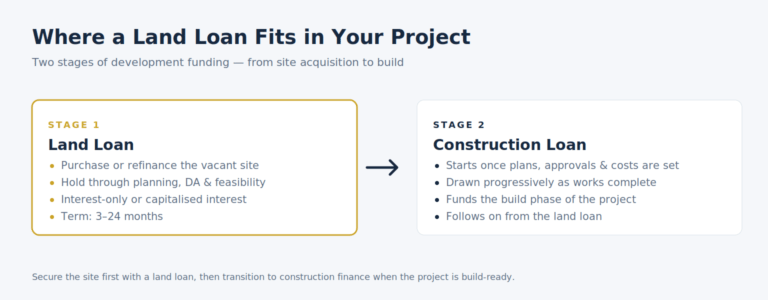

A land loan is typically the first stage of a broader property development loan strategy, and can be combined with a second mortgage loan to release additional equity for pre-development costs or to bridge between project stages.

| Key Features | Indicative Range |

|---|---|

| Loan amount | $250k – $10M+ (case-by-case) |

| Term | 3 – 24 months |

| LVR (metro residential) | Up to 75% (higher with DA in place) |

| LVR (rural / regional) | Up to 60% (case-by-case, depends on location & marketability) |

| Interest rate | From 8.5% p.a. (subject to LVR, security & exit strategy) |

| Repayment options | Interest-only or capitalised interest (structure varies by deal) |

| Income verification | Not required (asset-backed lending) |

| Typical timeframe | Indicative terms 1–2 business days • Settlement typically 5–10 business days (after valuation & required documents are received) |

All figures are indicative only and not an offer of finance. Availability, terms and timing are subject to valuation, security, lender approval, legal/settlement requirements and receipt of required documentation.

A vacant land loan is a loan secured against vacant land. It is commonly used when a borrower wants to purchase or refinance a site before there is a fixed building contract in place, or when the strategy is to hold the land while planning, zoning, feasibility or timing is being worked through. Depending on the lender and the scenario, land loans may suit borrowers looking at development site acquisition, land banking, refinance of existing vacant land, or early-stage site control ahead of the next funding phase.

Land loans are typically used to purchase or refinance vacant land before construction begins, with the assessment usually focused on the site itself, the proposed loan amount, the borrower structure and the planned exit strategy. In most cases, the lender will review the property details, the intended use of the land, the proposed loan to value ratio, and how the borrower expects to repay, sell or refinance the loan at the end of the term. If the application progresses, it usually moves through valuation, due diligence and formal credit assessment before settlement.

Banks and private lenders both offer land loans in Australia, but they assess vacant land very differently. Banks typically treat vacant land as a higher-risk security, which means larger deposits, full income verification and, in many cases, a requirement to build within a set timeframe. Private land loans are assessed on the asset and the exit strategy instead, which makes them better suited to developers, land bankers and borrowers who don’t fit standard bank criteria.

| Bank Land Loans | Private Land Loans (Formation Finance) | |

|---|---|---|

| Deposit / LVR | Usually 20–30% deposit required | Up to 75% LVR metro (up to 60% rural) |

| Interest rate | Lower rates, but strict eligibility | From 8.5% p.a., priced on risk & exit |

| Approval & settlement speed | Typically 4–8 weeks | Indicative terms in 1–2 days, settlement in 5–10 business days |

| Income verification | Full income & expense assessment required | Not required — asset-backed lending |

| Intention to build | Often required within 2–5 years | Not required — land banking welcome |

| Rural / regional land | Often restricted by postcode & land size | Considered case-by-case, including rural acreage |

| Best suited for | Owner-occupiers building soon | Developers, investors, land banking, fast settlements |

If you have strong income documentation, plan to build shortly and can wait for a longer approval process, a bank land loan may offer a lower rate. If speed, flexibility or a land banking strategy matters more, a private land loan is often the more practical path. All figures are indicative only and subject to valuation, security and lender approval.

A land loan may suit borrowers who need to secure a development site before moving into DA, detailed design or construction finance.

A land loan may also suit borrowers who want to hold a strategically located site while waiting for a clearer planning outcome, improved market timing or a later development stage.

Where a borrower already owns a site, land loans may be used to refinance existing debt, extend holding time or restructure a position ahead of the next stage.

In some cases, equity release against land may help fund early costs such as planning, reports, surveys, consultants or other site preparation expenses, subject to lender assessment.

We also fund vacant land loans for rural and regional sites, including acreage without development plans. Rural land is assessed case-by-case at up to 60% LVR, depending on location and marketability.

For land loans, we assess the asset quality and the clarity of the exit strategy. We want to understand how the loan will be repaid and whether the site is marketable within a realistic timeframe.

What we look at

Site fundamentals: location, access, shape, services (water/sewer/power), easements

Zoning & planning: zoning, overlays, permitted use, subdivision/development potential

Deal details: purchase price/valuation, contract terms, settlement timing

Security & leverage: proposed LVR, valuation approach, supporting security (if any)

Borrower profile: entity structure, relevant experience, overall capacity to execute

Exit strategy: sale, refinance after milestones, or next-stage funding pathway

Indicative terms are subject to valuation, due diligence, and final credit approval.

Borrower name(s) and entity type (individual, company, trust)

Directors/trustees details and ID (as required)

Current ownership structure and signing authority

Brief track record summary (prior projects, if any)

Land loans and construction loans are related, but they are not the same type of facility.

A land loan is usually used to purchase or refinance vacant land before construction funding is in place. A construction loan is generally used once the project moves into the building stage and the facility is drawn progressively as works are completed.

If the immediate need is to secure a site, a land loan may be the more suitable starting point. If the site is already controlled and the project is ready to move into build phase with plans, approvals, costs and delivery documentation, construction finance may be the more relevant next step.

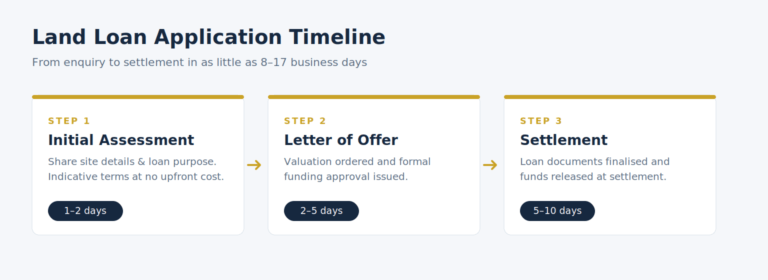

1. Initial assessment and Indicative Terms (1-2 days)

→ Share property details and loan purpose. Get indicative funding terms at no upfront costs.

2. Obtain final letter of offer (2-5 days)

→ Order valuation report and obtain funding approval.

3. Loan settlement (5-10 days)

→ Finalise loan documentation and receive funds/ property settlement.

Reviewed by Jackie Wang, Partner at Formation Finance

Jackie Wang holds a Master of Professional Accounting from the Royal Melbourne Institute of Technology (RMIT), and has over 10 years of experience in finance and lending, structuring tailored land loan solutions for Australian developers and investors.

Last update: 03/07/2026

Timeline for securing land loans from non-bank lenders can range from a few days to a few weeks.

When applying for a land loan, all you need to provide are the property address, your value estimate (subject to valuation report), loan amount required and loan purpose.

No. No income documentation or expenditure check is required.

Yes! We fund land banking – perfect for holding strategic sites until market conditions improve or rezoning/ Development Approval.

Banks typically require a 20–30% deposit for vacant land. With Formation Finance, we lend up to 75% LVR on metro residential land, meaning a deposit (or equity contribution) of around 25% — and up to 60% LVR on rural or regional land. Existing property equity can also be used to reduce the cash required.

From banks, yes. Vacant land is treated as higher-risk security, so banks apply larger deposits, stricter location and land-size rules, and often a requirement to build. Our land loans are assessed on the land asset and your exit strategy instead, with no income verification, which makes approval more straightforward for developers and investors.